Research News and Market Data on KTOS

Third Quarter 2024 Revenues of $275.9 Million Compared with Third Quarter 2023 Revenues of $274.6 Million

Third Quarter 2024 Unmanned Systems Revenues of $64.2 Million Compared with Third Quarter 2023 Revenues of $56.7 Million

Third Quarter 2024 Consolidated Book to Bill Ratio of 1.0 to 1 and Last Twelve Months Ended September 29, 2024

Consolidated Book to Bill Ratio of 1.1 to 1

Third Quarter 2024 Consolidated Bookings of $267.2 Million and Last Twelve Months Ended September 29, 2024 Consolidated Bookings of $1.240 Billion

Affirms Full Year 2024 Financial Forecast

SAN DIEGO, Nov. 07, 2024 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq:KTOS), a Technology Company in the Defense, National Security and Global Markets, today reported its third quarter 2024 financial results, including Revenues of $275.9 million, Operating Income of $6.5 million, Net Income of $3.2 million, Adjusted EBITDA of $24.6 million and a consolidated book to bill ratio of 1.0 to 1.0.

Included in third quarter 2024 Net Income and Operating Income is non-cash stock compensation expense of $7.2 million and Company-funded Research and Development (R&D) expense of $9.9 million.

Kratos reported third quarter 2024 GAAP Net Income attributable to Kratos of $3.2 million and Earnings Per Share of $0.02 compared to a GAAP Net Loss attributable to Kratos of $1.6 million and a GAAP Net Loss per share of $0.01 for the third quarter of 2023. Adjusted EPS was $0.11 for the third quarter of 2024 compared to $0.12 for the third quarter of 2023.

Third quarter 2024 Revenues of $275.9 million increased $1.3 million, or 0.5 percent, from third quarter 2023 Revenues of $274.6 million. Including the impact of the Sierra Technical Services, Inc. (STS) acquisition on a pro forma basis as if acquired at the beginning of 2023, Unmanned Systems reported 8.7 percent organic revenue growth. Kratos Turbine Technologies, Microwave Products, C5ISR, Defense Rocket Support and Training Solutions businesses in KGS also all reported organic revenue growth, offset by the previously reported and expected decline of approximately $24.2 million in the Space and Satellite business, primarily resulting from the industry related impact from OEM delays in the manufacture and delivery of software defined satellites.

Third quarter 2024 Cash Flow Generated from Operations was $6.1 million, which includes working capital requirements for increases in prepaid assets, inventory balances, vendor required deposits and reduction in deferred revenue or customer prepayment balances. Free Cash Flow Used in Operations was $9.2 million after funding of $15.3 million of capital expenditures, including the continued manufacture of two production lots of Kratos Valkyrie unmanned tactical jet drone aircraft prior to contract award.

For the third quarter of 2024, Kratos’ Unmanned Systems Segment (KUS) generated Revenues of $64.2 million, compared to $56.7 million in the third quarter of 2023, with organic revenue growth of 8.7 percent, driven primarily by increased target drone production, and reflects the pro forma impact of the STS acquisition as if acquired at the beginning of 2023. KUS’s Operating Income was $0.4 million in the third quarter of 2024 compared to Operating Income of $2.6 million in the third quarter of 2023, primarily reflecting the mix of revenues and resources.

KUS’s Adjusted EBITDA for the third quarter of 2024 was $3.6 million, compared to third quarter 2023 KUS Adjusted EBITDA of $5.4 million, reflecting the mix of revenues and resources.

KUS’s book-to-bill ratio for the third quarter of 2024 was 0.5 to 1.0 and 1.1 to 1.0 for the last twelve months ended September 29, 2024, with bookings of $32.6 million for the three months ended September 29, 2024, and bookings of $295.1 million for the last twelve months ended September 29, 2024. Total backlog for KUS at the end of the third quarter of 2024 was $273.9 million compared to $305.5 million at the end of the second quarter of 2024.

For the third quarter of 2024, Kratos’ Government Solutions Segment (KGS) generated Revenues of $211.7 million compared to $217.9 million in the third quarter of 2023, reflecting aggregate organic revenue increases of $18.0 million generated by the Kratos’ Turbine Technologies, Microwave Products, C5ISR, Defense Rocket Support and Training Solutions businesses in KGS, offset by the previously reported and expected decline of $24.2 million in the Space and Satellite business, as noted above.

KGS reported operating income of $13.5 million in the third quarter of 2024 compared to $15.9 million in the third quarter of 2023, primarily reflecting the revenue volume and mix of revenues and resources. Third quarter 2024 KGS Adjusted EBITDA was $21.0 million, compared to third quarter 2023 KGS Adjusted EBITDA of $22.3 million, reflecting the mix in revenues, revenue volume and resources.

For the third quarter of 2024 and the last twelve months ended September 29, 2024, KGS reported a book-to-bill ratio of 1.1 to 1.0, and bookings of $234.6 million and $945.0 million for the three and last twelve months ended September 29, 2024, respectively. KGS’s total backlog at the end of the third quarter of 2024 was $1.02 billion, as compared to $997.2 million at the end of the second quarter of 2024.

For the third quarter of 2024, Kratos reported consolidated bookings of $267.2 million and a book-to-bill ratio of 1.0 to 1.0, with consolidated bookings of $1.24 billion and a book-to-bill ratio of 1.1 to 1.0 for the last twelve months ended September 29, 2024. Consolidated backlog was $1.294 billion on September 29, 2024 and $1.303 billion on June 30, 2024. Kratos’ bid and proposal pipeline was $12.0 billion at September 29 and June 30, 2024. Backlog at September 29, 2024 was comprised of funded backlog of $1.098 billion and unfunded backlog of $195.4 million.

Eric DeMarco, Kratos’ President and CEO, said, “Kratos’ strategy of making internally funded investments, to be first to market with relevant hardware, software and systems, in coordination with our partners and customers is working, as reflected in our financial results and our $12 billion opportunity pipeline. A recent representative example of this success is the successful flight of Kratos’ Zeus 1 and Zeus 2 system solid rocket motor stack with our customer’s payload, positioning Kratos for potential growth above our current future revenue year over year 10% target beginning in 2026.”

Mr. DeMarco went on, “Consistent with the success of and opportunities from Kratos’ strategy, earlier this year we completed an equity raise to position the Company to ensure successful execution on programs we have received and expect to receive. As an update to the related investments we are making: Kratos is currently manufacturing ~ 165 jet drones a year and we are now positioned to increase to ~400 a year including Valkyrie. Kratos can now produce ~10,000 small jet engines annually for drones and missiles, Kratos Microwave Electronics’ expansion in Israel is on track for a Q2 2025 completion, including an additional new manufacturing facility, an expanded existing manufacturing facility and a space & satellite qualified capability; we have identified the site for our new rocket system production and integration facility including for Zeus, Oriole and Erinyes and plan to break ground by the end of this year; and we have now identified the site for our new turbofan engine facility. Importantly, each of these expansion initiatives have existing programs, customer funded backlog or opportunities, or are in conjunction with a partner.”

Mr. DeMarco continued, “We continue to make progress in Kratos’ tactical drone business, with Kratos’ Apollo drone program now in contract documentation and Kratos’ Athena drone program under contract. Additionally, we have had recent successful Valkyrie flights with the U.S. Marines, Navy and Office of the Secretary of Defense, and Kratos recently has been selected on a new tactical drone opportunity. Importantly, our Ghost Works is on track to fly both a Kratos tactical drone and Kratos target drone in 2025 with Kratos internally funded, developed and manufactured jet engines, which will provide increased performance and electrical power, at reduced cost. Kratos Ghost Works is also expecting to fly the newest version of Kratos Valkyrie in 2025, as we make internally funded investments and continue to expand the Valkyrie families’ capability set and further drive down its operating and overall cost, and our newest 5th Generation drone is also scheduled for first flight in 2025 in conjunction with our customer.”

Mr. DeMarco concluded, “We are in a generational recapitalization of strategic weapon systems, with Kratos being an industry leader in hardware, software and systems for mission critical National Security and Defense applications. Expected growth drivers for Kratos in 2025 include; Kratos Erinyes, Zeus, Dark Fury, Oriole and other relevant rocket systems; Kratos jet engine and propulsion systems for missiles, drones, supersonic and space systems; microwave electronics and C5ISR products for air defense, CUAS, missile and radar systems and jet target drone systems.”

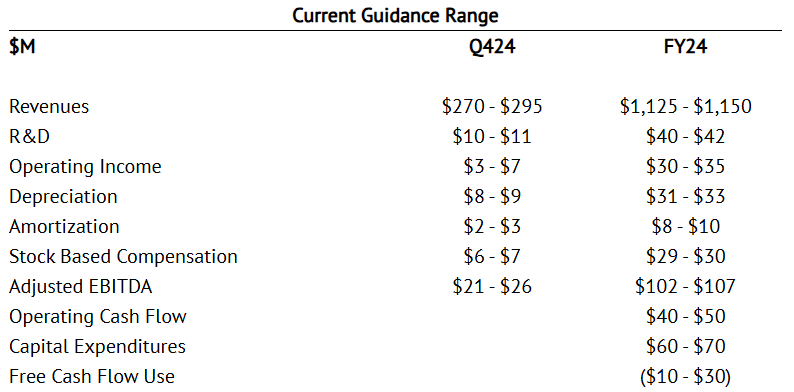

Financial Guidance

We are providing our initial 2024 fourth quarter financial guidance and affirming our full year 2024 guidance today, which ranges include our current forecasted business mix assumptions and expected contract execution and delivery schedules. Our financial guidance also includes our expectations and assumptions for our supply chain’s execution, and for employee sourcing, hiring, retention and related costs. We have also taken into consideration in our affirmed fiscal 2024 guidance the Federal Fiscal Year 2025 Continuing Resolution Authorization (CRA) which began on October 1, 2024, and under such expected CRA, no new program or contract awards, no increases in existing production contract funding, and no transition from program development to production are expected.

Our fourth quarter and full year 2024 guidance ranges are as follows:

For Kratos’ Fiscal year 2025, we are currently forecasting base case Revenue growth of approximately 10%, and Adjusted EBITDA growth. Our industry is currently operating under a Federal Fiscal Year 2025 CRA, which began October 1, 2024 and which is currently expected to continue into Kratos’ Fiscal 2025. There was also an approximate 6-month Federal Fiscal 2024 CRA, which was previously resolved in March 2024, Kratos’ current 2024 fiscal year. Additionally, the recent election will impact the Administration, House and Senate. Accordingly, we will be providing our detailed 2025 Revenue, Adjusted EBITDA, Cash Flow and other financial forecast information and guidance when we report our Fiscal 2024 results, currently expected to be in late February 2025. This will provide Kratos additional time to assess the impacts of these ongoing and recent events, if any, on National Security priorities, our 2025 business mix, contractual and program funding and timing assumptions and potential fiscal year 2025 fiscal quarter to quarter impacts. Kratos’ base case financial forecast does not assume or include any potential tactical drone program production.

Management will discuss the Company’s financial results, on a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern) today. The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions

Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com

Notice Regarding Forward–Looking Statements

This news release contains certain forward-looking statements that involve risks and uncertainties, including, without limitation, express or implied statements concerning the Company’s expectations regarding its future financial performance, including the Company’s expectations for its fourth quarter and full year 2024 and fiscal year 2025 revenues, revenue growth, Adjusted EBITDA growth, organic revenue growth rates, R&D, operating income (loss), depreciation, amortization, stock based compensation expense, and Adjusted EBITDA, and full year 2024 operating cash flow, capital expenditures and other investments, and free cash flow, the Company’s future growth trajectory and ability to achieve improved revenue mix and profit in certain of its business segments and the expected timing of such improved revenue mix and profit, including the Company’s ability to achieve sustained year over year increasing revenues, profitability and cash flow, the Company’s expectation of ramp on projects and that investments in its business, including Company funded R&D expenses and ongoing development efforts, will result in an increase in the Company’s market share and total addressable market and position the Company for significant future organic growth, profitability, cash flow and an increase in shareholder value, the Company’s bid and proposal pipeline and backlog, including the Company’s ability to timely execute on its backlog, demand for its products and services, including the Company’s alignment with today’s National Security requirements and the positioning of its C5ISR and other businesses, planned 2024 investments, including in the tactical drone and satellite areas, and the related potential for additional growth in 2025 and beyond, ability to successfully compete and expected new customer awards, including the magnitude and timing of funding and the future opportunity associated with such awards, including in the target and tactical drone and satellite communication areas, performance of key contracts and programs, including the timing of production and demonstration related to certain of the Company’s contracts and control (TT&C) product offerings, the impact of the Company’s restructuring efforts and cost reduction measures, including its ability to improve profitability and cash flow in certain business units as a result of these actions and to achieve financial leverage on fixed administrative costs, the ability of the Company’s advanced purchases of inventory to mitigate supply chain disruptions and the timing of converting these investments to cash through the sales process, benefits to be realized from the Company’s net operating loss carry forwards, the availability and timing of government funding for the Company’s offerings, including the strength of the future funding environment, the short-term delays that may occur as a result of Continuing Resolutions or delays in U.S. Department of Defense (DoD) budget approvals, timing of LRIP and full rate production related to the Company’s unmanned aerial target system offerings, as well as the level of recurring revenues expected to be generated by these programs once they achieve full rate production, market and industry developments, and the current estimated impact of the national election, supply chain disruptions, availability of an experienced skilled workforce, inflation and increased costs, risks related to potential cybersecurity events or disruptions of our information technology systems, and delays in our financial projections, industry, business and operations, including projected growth. Such statements are only predictions, and the Company’s actual results may differ materially from the results expressed or implied by these statements. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and the Company undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Factors that may cause the Company’s results to differ include, but are not limited to: risks to our business and financial results related to the reductions and other spending constraints imposed on the U.S. Government and our other customers, including as a result of sequestration and extended continuing resolutions, the Federal budget deficit and Federal government shut-downs; risks of adverse regulatory action or litigation; risks associated with debt leverage; risks that our cost-cutting initiatives will not provide the anticipated benefits; risks that changes, cutbacks or delays in spending by the DoD may occur, which could cause delays or cancellations of key government contracts; risks of delays to or the cancellation of our projects as a result of protest actions submitted by our competitors; risks that changes may occur in Federal government (or other applicable) procurement laws, regulations, policies and budgets; risks of the availability of government funding for the Company’s products and services due to performance, cost growth, or other factors, changes in government and customer priorities and requirements (including cost-cutting initiatives, the potential deferral of awards, terminations or reduction of expenditures to respond to the priorities of Congress and the Administration, or budgetary cuts resulting from Congressional committee recommendations or automatic sequestration under the Budget Control Act of 2011, as amended); risks that the unmanned aerial systems and unmanned ground sensor markets do not experience significant growth; risks that products we have developed or will develop will become programs of record; risks that we cannot expand our customer base or that our products do not achieve broad acceptance which could impact our ability to achieve our anticipated level of growth; risks of increases in the Federal government initiatives related to in-sourcing; risks related to security breaches, including cyber security attacks and threats or other significant disruptions of our information systems, facilities and infrastructures; risks related to our compliance with applicable contracting and procurement laws, regulations and standards; risks related to the new DoD Cybersecurity Maturity Model Certification; risks relating to the ongoing conflict in Ukraine and the Israeli-Palestinian military conflict; risks to our business in Israel; risks related to our international operations; risks related to contract performance; risks related to failure of our products or services; risks associated with our subcontractors’ or suppliers’ failure to perform their contractual obligations, including the appearance of counterfeit or corrupt parts in our products; changes in the competitive environment (including as a result of bid protests); failure to successfully integrate acquired operations and compete in the marketplace, which could reduce revenues and profit margins; risks that potential future goodwill impairments will adversely affect our operating results; risks that anticipated tax benefits will not be realized in accordance with our expectations; risks that a change in ownership of our stock could cause further limitation to the future utilization of our net operating losses; risks that we may be required to record valuation allowances on our net operating losses which could adversely impact our profitability and financial condition; risks that the current economic environment will adversely impact our business, including with respect to our ability to recruit and retain sufficient numbers of qualified personnel to execute on our programs and contracts, as well as expected contract awards and risks related to increasing interest rates and risks related to the interest rate swap contract to hedge Term SOFR associated with the Company’s Term Loan A; and risks related to natural disasters or severe weather. These and other risk factors are more fully discussed in the Company’s Annual Report on Form 10-K for the period ended December 31, 2023, and in our other filings made with the Securities and Exchange Commission.

Note Regarding Use of Non-GAAP Financial Measures and Other Performance Metrics

This news release contains non-GAAP financial measures, including organic revenue growth rates, Adjusted EPS (computed using income from continuing operations before income taxes, excluding income (loss) from discontinued operations, excluding income (loss) attributable to non-controlling interest, excluding depreciation, amortization of intangible assets, amortization of capitalized contract and development costs, stock-based compensation expense, acquisition and restructuring related items and other, which includes, but is not limited to, legal related items, non-recoverable rates and costs, and foreign transaction gains and losses, less the estimated impact to income taxes) and Adjusted EBITDA (which includes net income (loss) attributable to noncontrolling interest and excludes, among other things, losses and gains from discontinued operations, acquisition and restructuring related items, stock compensation expense, foreign transaction gains and losses, and the associated margin rates). Additional non-GAAP financial measures include Free Cash Flow from Operations computed as Cash Flow from Operations less Capital Expenditures plus proceeds from sale of assets and Adjusted EBITDA related to our KUS and KGS businesses. Kratos believes this information is useful to investors because it provides a basis for measuring the Company’s available capital resources, the actual and forecasted operating performance of the Company’s business and the Company’s cash flow, excluding non-recurring items and non-cash items that would normally be included in the most directly comparable measures calculated and presented in accordance with GAAP. The Company’s management uses these non-GAAP financial measures, along with the most directly comparable GAAP financial measures, in evaluating the Company’s actual and forecasted operating performance, capital resources and cash flow. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information presented in compliance with GAAP, and investors should carefully evaluate the Company’s financial results calculated in accordance with GAAP and reconciliations to those financial results. In addition, non-GAAP financial measures as reported by the Company may not be comparable to similarly titled amounts reported by other companies. As appropriate, the most directly comparable GAAP financial measures and information reconciling these non-GAAP financial measures to the Company’s financial results prepared in accordance with GAAP are included in this news release.

Another Performance Metric the Company believes is a key performance indicator in our industry is our Book to Bill Ratio as it provides investors with a measure of the amount of bookings or contract awards as compared to the amount of revenues that have been recorded during the period and provides an indicator of how much of the Company’s backlog is being burned or utilized in a certain period. The Book to Bill Ratio is computed as the number of bookings or contract awards in the period divided by the revenues recorded for the same period. The Company believes that the rolling or last twelve months’ Book to Bill Ratio is meaningful since the timing of quarter-to-quarter bookings can vary.

Press Contact:

Yolanda White

858-812-7302 Direct

Investor Information:

877-934-4687

[email protected]