Looking Back at the Markets in June and Forward to July

Enthusiasm in the overall stock market was strong in June, the major indices were all up, and every S&P sector closed in positive territory. In fact, there was spectacular performance across market caps as Apple (AAPL) became the first company to reach a $3 trillion market cap, and noteworthy among small caps, Bitcoin mining company Bit Digital (BTBT) was up another 20% and a staggering 685% on the year during the last week in June. The across-the-board positive sentiment came during a month when the market was disappointed by the Federal Reserve’s continued hawkish bias.

Two dark clouds that the markets had hanging over them as they entered June were a possible U.S. default on debt and talk of a recession later this year. A higher debt ceiling law was signed on June 5, and a strong jobs report and higher-than-expected first-quarter GDP have for most, pushed most recession forecasts into 2024 or later. June’s performance may reflect a celebration and feelings of relief from both concerns.

Consumer confidence improved in June to its highest level since January 2022, reflecting a big jump in outlook and expectations. This surprise positive mood is reflected in stock market rotations experienced during June in both market-cap and market sectors.

Look Back

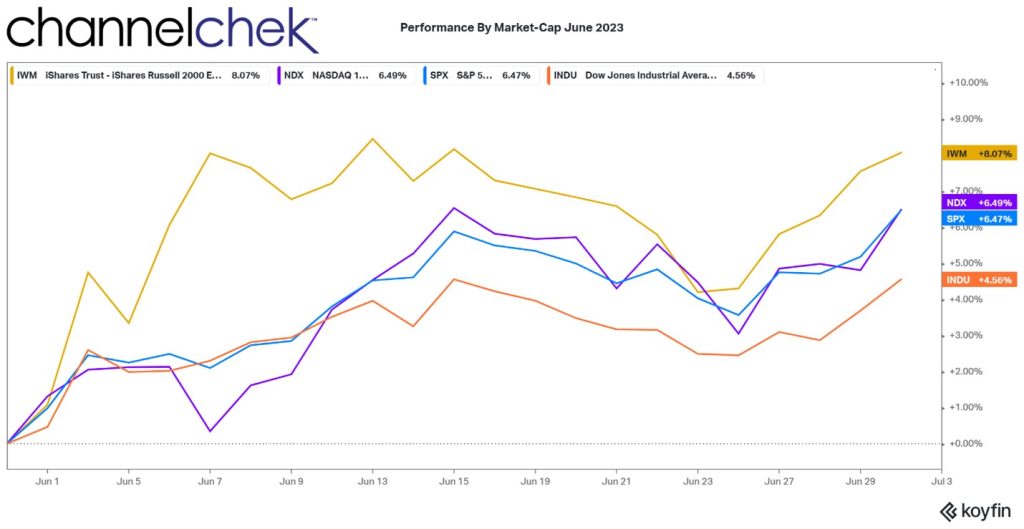

Four broad stock market indices were positive in June. In order, the Russell 2000 Small Caps, Nasdaq 100 Large Caps, the S&P 500 Large Caps, and the Dow Jones Industrials. Small cap stocks are the big winner in June as investors went looking for value. The Russell 2000 rose 8.07%. The smaller stocks may now have more positive impetus that could carry over into July as a report released last week by Goldman Sachs estimates that based on their models, small cap stocks could rise 14% over the next 12 months.

While small cap stocks had their stars, the Nasdaq maintained a startling pace as big tech retained its appeal despite individual company market caps that have exceeded those of developed countries. The Nasdaq 100 was up 6.49% in June. The S&P 500 nearly matched Nasdaq with a 6.47% return. The Dow 30 Industrials, which have had a difficult few months, returned 4.56% to investors.

Market Sector Lookback

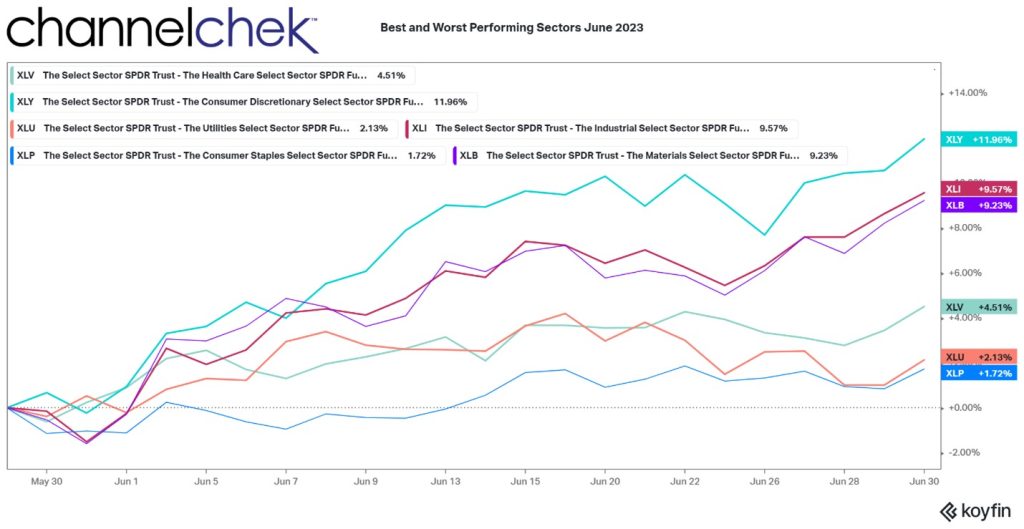

Of the 11 S&P market sectors (SPDRs), even the lowest performer had an impressive one-month return. The chart above reflects the three best-performing sectors and the three worst. The performance indicates that there was a sector rotation away from defensive stocks during June.

Consumer Discretionary had the best return at 11.96%. By definition, these are companies selling products that consumers can cut back on or more easily avoid. The top ten holdings include Starbucks (SBUX), Bookings Holdings (BKNG), and Tesla (TSLA).

What S&P calls the Industrial Select sector finally came to life in June. Its 9.57% return represents almost all of this sector’s performance for the first six months of 2023 (9.73% YTD). Examples of top stocks contained in this index are John Deere (D.E.), General Electric (G.E.), and Union Pacific (UNP).

The third was Materials Select which was negative on the year heading into June. The 9.23% return on the month more than erased the negative 7.67% performance heading into the month.

Each of the top three performers is typically sectors that investors delve into when their economic outlook is more positive.

The three worst-performing sectors also indicate the month was very positive. The Health Care sector was the best of the bottom three at 4.51%. While this did not bring the sector positive on the year, companies like Johnson & Johnson (JNJ), Abbott Labs (ABT), and United Health (UNH), had experienced strong years this decade with growth drivers that have since weakened some.

The second to weakest performer is Utilities Select. Utilities are still negative on the year despite a 2.13% increase in June. Companies like American Electric Power (AEP), Dominion Energy (D), and Consolidated Edison (E.D.) are surrounded by a lot of uncertainty as their costs are driven more than other industries by fuel prices. Additionally, investors in utilities tend to be dividend stock investors. Dividend stocks tend to underperform in a rising interest rate environment as they compete less favorably with bonds.

The worst-performing sector provides further evidence of a rotation during June. Consumer Staples was the second-worst-performing sector at the close of May. While it returned 1.72% in June, the sector, which includes Colgate Palmolive (CL), Walmart (WMT), and Philip Morris (PM), usually gains in popularity when consumer confidence is low, it loses popularity as consumer confidence is high, that’s when, as we saw in June, consumer discretionary stocks get attention.

Looking Forward

The job market is strong, inflation is tapering, and consumers are more confident. There are even signs that companies that have been waiting for an improved market to go public are considering now a good time for an IPO.

Bitcoin mining stocks and artificial intelligence are still be on fire. The crypto-mining stocks interest is tied to the price of Bitcoin – many of the stocks have actually outperformed the cryptocurrency. Artificial intelligence, as its potential becomes better understood, has inspired many to place bets that this will grow into a technology that is indispensable to many industries. Is the next Apple in this tech segment?

The rotation to small caps and sectors that perform better when the economy improves has a lot of momentum heading into July.

The next FOMC meeting is July 25-26; while market participants already expect further tightening, it has not deterred their positive view on the “risk-on” trade.

Take-Away

The market was jubilant in June. The signing into law of an increased debt ceiling helped kick off a change from the uncertain mood in May. It unleashed buyers that continued even after it was clear the Federal Reserve was not finished hiking interest rates.

The year 2023 now sits at the halfway point. And within a few months, we will be in a presidential election year. Stocks tend to do well in election years. While the Russia/Ukraine situation is still uncertain, especially in the energy sector, the markets seem to have already priced in negative scenarios and are marching upward confidently.

Managing Editor, Channelchek